-

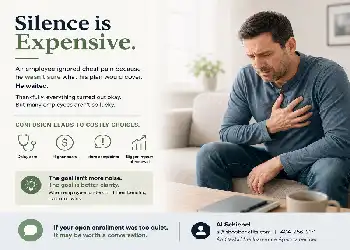

A few days ago, I received a call from an employee at one of my client’s companies. She sounded frustrated. “Al, my doctor’s office told me they accepted our insurance… so why did I get this bill?” It turned out she’d done exactly what most people would do. Before scheduling her appointment, she called the…

-

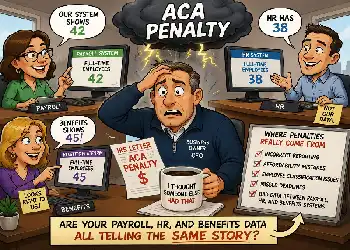

A business owner said something to me recently that I’ve heard more times than I can count. He leaned back in his chair, crossed his arms, and said: “We should be okay. I think payroll handles all of that.” I didn’t answer right away. It wasn’t the word “payroll” that caught my attention. It was…

-

The Hidden Danger in Your Benefits Plan: The Power of Assumptions I was sitting across the table from a referred HR director recently when she smiled and said, “I think we’re in pretty good shape.” I asked a simple question. “Who handles your benefits compliance?” Without hesitation she answered, “Our carrier.” I asked another question.…

-

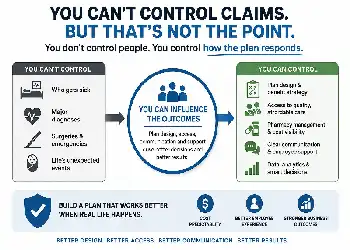

You Can’t Control Claims—But You Are Worrying About the Wrong Variable Recently, I was sitting across from a business owner who was incredibly frustrated. His corporate health insurance renewal premiums had jumped significantly yet again, and he felt completely defeated. He looked at me and said, “Al, I just don’t know what else to do.…

-

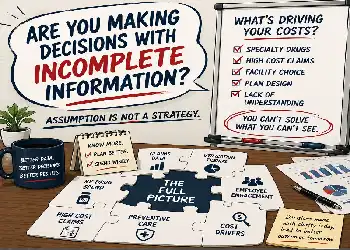

Assumption is Not a Strategy: Are You Making Benefits Decisions with Incomplete Information? A few years ago, I sat down with a company owner who was visibly frustrated about facing yet another double-digit health insurance renewal increase. He was entirely convinced that the insurance carrier was simply squeezing his business. His exact words to me…

-

Why a Quiet Open Enrollment is Actually a Warning Sign During open enrollment, no news is generally taken as good news. Human resources teams breathe a sigh of relief when the deadline passes without a flood of frantic emails or phone calls. But after years of managing corporate benefits programs, we have learned a hard…

-

When business leaders look at their annual healthcare spend, they tend to focus on the big numbers: total claims paid, premium spikes, and renewal percentages. But here is an overlooked reality of corporate benefits management: most of the expensive decisions employees make with their health plan don’t happen when a claim is filed. They happen…

-

Is Your Health Insurance Renewal Meeting Lying to You? Every year, business leaders gather around a conference table for the annual health insurance renewal meeting. The atmosphere is usually a mix of anticipation and dread. But here is a hard truth about that meeting: it is lying to you a little. This isn’t because your…