You Can’t Control Claims

You Can’t Control Claims—But You Are Worrying About the Wrong Variable

Recently, I was sitting across from a business owner who was incredibly frustrated. His corporate health insurance renewal premiums had jumped significantly yet again, and he felt completely defeated. He looked at me and said, “Al, I just don’t know what else to do. We can’t control medical claims.”

I nodded in agreement, because he is absolutely right. Any benefits strategy that depends on controlling the health events of your workforce is fundamentally flawed.

You cannot control who receives a devastating cancer diagnosis. You cannot control which employee will eventually require a major knee replacement, or who will experience a complicated, premature birth. Trying to control people’s health is a losing battle. But then, I asked him a completely different question:

“What if claims aren’t the variable you’re actually supposed to be controlling?”

That single question completely shifted the conversation.

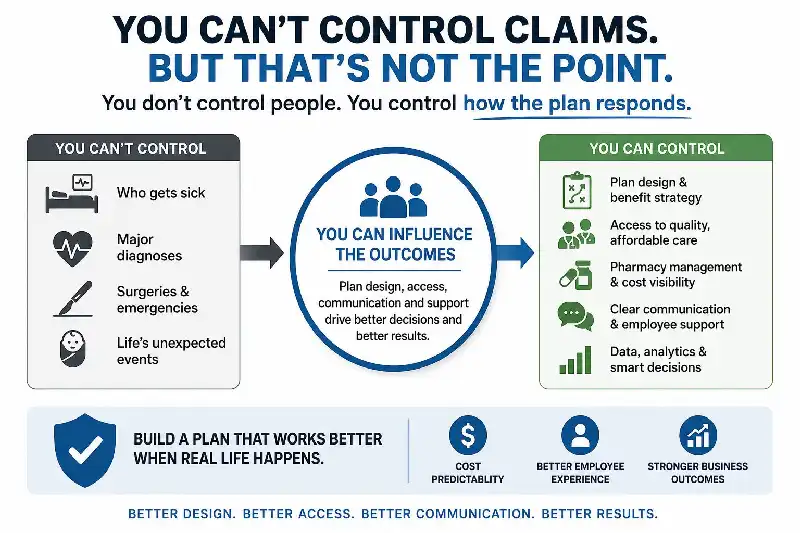

Shifting Your Focus From the Outcome to the System

While you cannot control the onset of a medical claim, you can completely control **how your health insurance plan responds to it.** Most employers spend an enormous amount of time stressing over the final financial outcome instead of managing the underlying system that creates that outcome.

The businesses that consistently achieve stable rates and better results aren’t just lucky—they are highly intentional. They implement mechanisms to actively influence how the plan operates in the real world:

- Directing Care: You can guide employees toward high-quality, lower-cost healthcare options before they make an expensive decision.

- Enhancing Primary Care Access: You can make routine, preventive primary care highly accessible so small health issues are caught early.

- Managing Pharmacy Trends: You can closely monitor emerging prescription medication utilization before it snowballs into a major budgetary surprise.

- Supporting Smarter Choices: You can provide clear, timely communication so employees feel confident navigating the system when real-life health events happen.

The goal of a modern, strategic benefits program isn’t to police your workforce. The goal is to build a well-designed framework that works efficiently and cost-effectively the moment an unexpected health event occurs.

Stop Reacting, Start Managing

If you have ever looked at your annual renewal increase and thought, “There has to be a better way than just raising deductibles and hoping for the best,” you are ready for a systematic shift. Let’s stop trying to control claims and start controlling how your plan handles them.

Connect with Al Schiebel today:

- Email: al@shopbenefits.com

- Phone: 404-256-2171

ShopBenefits is an Oakbridge Insurance Agency partner.