Your Health Plan Costs Went Up Again

If You Can’t Explain It, You Can’t Control It

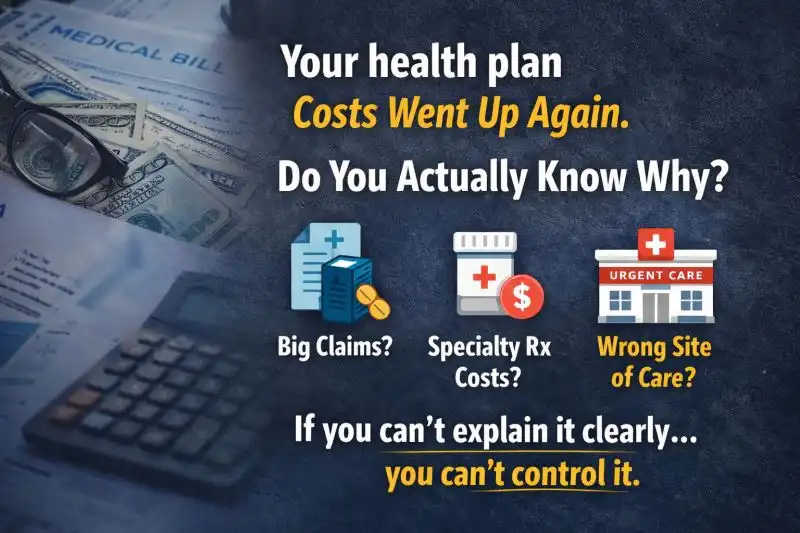

Your health plan costs went up again. But do you actually know why? I’m not talking about the “polished” answer your broker might give you—the vague references to “market trend,” “utilization,” or “the general economy.” I mean the real reason.

In most companies, the renewal process follows a predictable, passive script: a renewal shows up, a few slides are presented with big-picture talking points, and everyone just kind of… accepts it. But if you can’t clearly explain exactly what changed, where the claims are originating, and what behavior is driving those costs, you aren’t actually managing your plan. You’re simply reacting to it.

This reactive cycle is where things get expensive. This isn’t just about the bottom line; your benefits strategy touches everything from employee retention and morale to the way your team accesses care. When employees don’t understand how the plan works, they naturally make poor decisions—not intentionally, but out of confusion.

That confusion shows up in your numbers. The real issue usually isn’t “the market.” It’s specific, manageable factors: a few large claims skewing the data, specialty Rx quietly driving spend, or employees using the wrong sites of care because they don’t know any better.

None of these issues are fixed with a standard benchmark report. The employers who handle benefits well don’t just chase the cheapest plan every year. Instead, they take control. They understand their data, they communicate with their team year-round, and they actively influence how the plan is used (in a HIPAA-compliant way, of course).

That is the secret to making renewals stop feeling like an annual ambush. If you can’t explain your plan clearly, you can’t control it.

I’m curious: What is the “polished” explanation you usually hear when your costs go up? Let’s talk about the real reasons instead.